Converting a manufactured home from personal property to real property is one of the most financially impactful things a manufactured homeowner can do. This process — sometimes called titling or deeding your manufactured home — changes how the home is classified legally, which unlocks better financing options, lowers your interest rate, and can meaningfully increase your home’s value.

In this step-by-step guide, we explain exactly what the conversion process involves, who qualifies, how much it costs, and how to navigate the process in your state.

What Does Converting to Real Property Mean?

When a manufactured home is purchased and placed on leased land, it is typically titled as personal property — the same legal category as a vehicle. A certificate of title is issued by your state’s motor vehicle department or equivalent agency, similar to a car title.

When you convert the home to real property, you change its legal classification from vehicle-like to real estate. The home is attached permanently to land you own, the certificate of title is surrendered and cancelled, and the home becomes part of the real estate — recorded with your county’s land records as a deed.

Why Convert? The Benefits Are Significant

Access to Mortgage Financing

The most important benefit. Once your manufactured home is real property, you can finance it with a real mortgage — including FHA Title II, VA, USDA, and conventional loans. Mortgage interest rates are typically 2 to 5 percentage points lower than chattel loan rates. On a $150,000 balance, that difference can mean $200 to $400 less per month.

Higher Property Value

Real property is generally appraised and valued more favorably than personal property. Converting to real property can increase your home’s appraised value by 10 to 25 percent in many markets.

Equity Building

Because real property mortgages amortize differently from chattel loans — longer terms, lower rates — you build equity faster. Combined with land appreciation, a converted manufactured home can build wealth meaningfully over time.

Better Insurance Rates

In many states, manufactured homes classified as real property qualify for homeowner’s insurance rather than manufactured home insurance, which can be cheaper and offer broader coverage.

Requirements for Conversion

1. You Must Own the Land

This is the fundamental requirement. You cannot convert a manufactured home to real property if it is on leased land in a park. The home and the land must be owned by the same person or persons.

2. The Home Must Be Permanently Affixed

The home must be attached to a permanent foundation — typically a continuous concrete perimeter foundation, concrete piers, or a combination. The transportation undercarriage (wheels, axles, hitch) must be removed.

3. HUD Compliance

The home must have been built to HUD Manufactured Home Construction and Safety Standards (built after June 15, 1976) and must have its HUD certification labels attached.

4. Clear Title

There can be no outstanding liens on the manufactured home title other than a purchase loan that will be paid off at conversion.

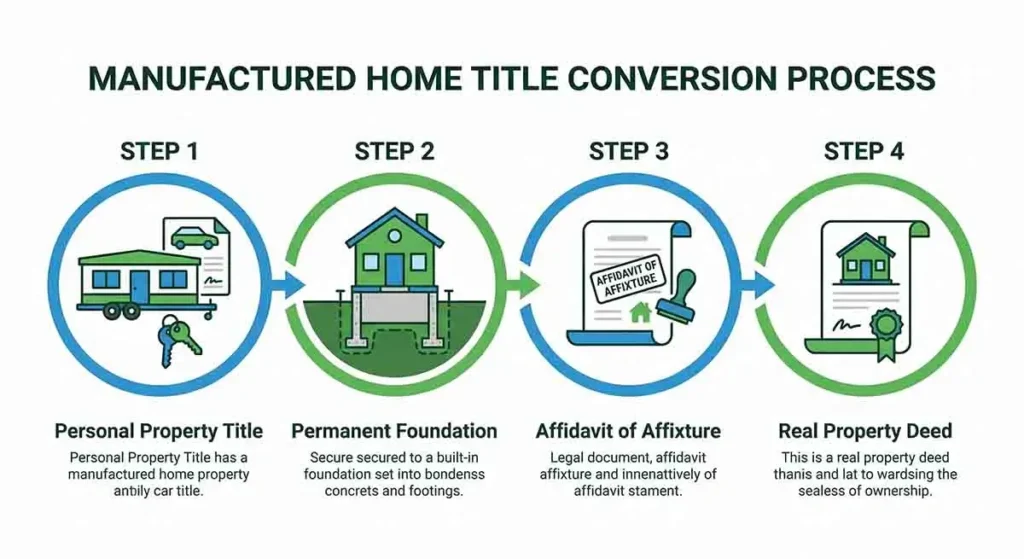

Step-by-Step Conversion Process

Step 1: Confirm You Meet the Requirements

Before starting, confirm that you own the land, the home is on a permanent foundation, the HUD tags are present, and the title is clear of liens.

Step 2: Contact Your State Housing Agency or DMV

In most states, the conversion process starts with the agency that currently holds the manufactured home title. Contact them to get state-specific forms and instructions for surrendering the title.

Step 3: Get an Engineer’s Certification (If Required)

Many lenders and some states require a licensed engineer to inspect and certify that the manufactured home is on a permanent foundation meeting HUD standards. This inspection typically costs $300 to $600.

Step 4: Prepare the Affidavit of Affixture

Most states require an Affidavit of Affixture or similar document declaring the home is permanently attached to the land. This document is notarized and filed with your county recorder’s office.

Step 5: Surrender the Certificate of Title

Submit the original certificate of title, the affidavit of affixture, and any required forms to the appropriate state agency. Fees typically range from $50 to $500.

Step 6: Record the Deed

Once the title is cancelled, your deed must be recorded with your county recorder to document the real property status. Recording fees are typically $50 to $200.

Step 7: Update Your Insurance and Tax Records

After conversion, contact your insurance company to update your policy, and notify your county tax assessor of the change in classification.

How Long Does the Conversion Take?

The conversion process typically takes 4 to 12 weeks from start to finish, depending on your state and whether there are any complications. States like Texas and Florida have streamlined the process. If you are converting as part of a purchase transaction, your lender and title company will manage much of the process.

How Much Does the Conversion Cost?

Total conversion costs typically range from $500 to $3,000, depending on your state and whether you hire professional help:

- Foundation inspection and engineer certification: $300 to $600

- Title cancellation fees: $50 to $500

- Affidavit preparation (attorney or title company): $200 to $500

- County recording fees: $50 to $200

- Miscellaneous (notary, title search): $100 to $300

If your foundation needs to be upgraded to meet HUD permanent foundation standards, that can add $3,000 to $15,000 or more — but it is a one-time expense that provides lasting financial benefits.

State-Specific Considerations

The conversion process and requirements vary by state. Texas, Florida, North Carolina, and California have established, relatively straightforward conversion processes. Others have more complicated procedures.

We strongly recommend contacting your state’s manufactured housing authority or an experienced local real estate attorney who has handled manufactured home conversions before starting the process.

The Bottom Line

Converting a manufactured home from personal property to real property is one of the best financial moves a manufactured homeowner can make. The access to mortgage financing alone — with interest rates 2 to 5 points lower than chattel loans — can save tens of thousands of dollars over the life of the loan.

If you own a manufactured home on land you also own, and the home is not yet converted to real property, this should be near the top of your financial to-do list.

Darnell J. Okafor is a former housing attorney and legal aid lawyer who spent nine years representing manufactured home residents in Texas. He writes about tenant rights, eviction law, title issues, and legal protections for OwnedNotOwned.com — bringing attorney-level knowledge to readers who need clear answers.