One of the first questions buyers ask when researching manufactured home financing is: what credit score do I need to buy a manufactured home? The answer is not one single number — it depends on the type of loan you are applying for, the lender you choose, and whether the home is in a park or on land you own.

This guide gives you the specific credit score requirements for every major manufactured home loan type, explains what lenders look at beyond just your score, and provides practical steps to improve your credit before applying.

Credit Score Requirements by Loan Type

FHA Loans (Title I and Title II)

FHA loans are the most flexible government-backed option for manufactured home buyers:

- Minimum credit score: 500 (with 10% down payment)

- Best terms start at: 580 (with 3.5% down payment)

- Lender reality: Most FHA lenders require 580 to 620 minimum in practice

VA Loans (Veterans)

VA loans for manufactured homes are available to eligible veterans and active-duty military:

- VA minimum: The VA itself does not set a minimum credit score

- Lender reality: Most VA lenders require 580 to 620 minimum

- Best rates typically start at: 660+

USDA Rural Development Loans

USDA loans are for rural properties and can be used for manufactured homes on owned land in eligible areas:

- Minimum credit score: 640 for automated underwriting approval

- Manual underwriting: 580+ with additional documentation

- Income limits apply — household income cannot exceed 115% of area median income

Conventional Loans (Fannie Mae and Freddie Mac)

Conventional loans for manufactured homes exist through Fannie Mae’s MH Advantage program and Freddie Mac’s CHOICEHome program:

- Minimum credit score: 620 (Fannie Mae MH Advantage)

- Best terms: 680+

- Home must meet specific design standards and be on owned land with permanent foundation

Chattel Loans (For Park Homes)

Chattel loans are personal property loans used when the home is in a park on leased land:

- Minimum credit score: Varies by lender — some specialty lenders go as low as 575

- 21st Mortgage Corporation and Vanderbilt Mortgage can work with lower scores with larger down payments

- Typical rate premium: 2 to 5 percent higher interest rate than equivalent mortgage loans

What Lenders Look at Beyond Your Credit Score

Debt-to-Income Ratio (DTI)

DTI is the percentage of your gross monthly income that goes to debt payments. Most lenders want:

- Front-end DTI (housing costs only): 28 to 31%

- Back-end DTI (all debts): 41 to 45%

Even with a strong credit score, a high DTI can get your application denied. Paying down existing debts before applying improves your DTI.

Employment and Income Stability

Lenders typically want 2 years of stable employment history. Self-employed applicants must provide 2 years of tax returns. Recent job changes — especially to a different industry — can complicate approval.

Down Payment

- 3.5% down: Available with FHA at 580+

- 10% down: Opens options for scores as low as 500 (FHA)

- 20% or more down: May unlock conventional options for scores in the 620 to 640 range

Home Age and Condition

Most FHA and conventional lenders will not finance homes older than 20 to 25 years. Chattel lenders vary — some specialty lenders will finance older homes with higher down payments and rates.

How to Check Your Credit Score for Free

Before applying for any manufactured home loan, know exactly where your credit stands:

- AnnualCreditReport.com — free official reports from all three bureaus once per year (now weekly through 2026)

- Credit Karma — free TransUnion and Equifax scores, updated regularly

- Your bank or credit card — many now provide free FICO scores to cardholders

Check all three credit bureau reports, not just one. Errors on one bureau’s report may not appear on others.

How to Improve Your Credit Score Before Applying

1. Pay Down Credit Card Balances (Fastest Impact)

Credit utilization — the percentage of your credit card limits that you are using — accounts for about 30% of your credit score. Getting your utilization below 30% (and ideally below 10%) can raise your score significantly, often within 30 to 60 days of the balance drop being reported.

2. Dispute Credit Report Errors

Review your reports carefully for accounts that are not yours, late payments you believe were on time, and balances that are higher than actual. Dispute errors directly with each credit bureau. Successful disputes can raise your score by 20 to 50 points.

3. Do Not Close Old Accounts

The length of your credit history accounts for about 15% of your score. Closing old accounts shortens your average account age. Even if you do not use an old credit card, keep it open with a small occasional charge to keep it active.

4. Avoid New Credit Applications

Each credit application results in a hard inquiry, which can temporarily lower your score by 5 to 10 points. Avoid applying for new credit in the 6 to 12 months before applying for your manufactured home loan.

5. Become an Authorized User

If a family member has a credit card with a long history of on-time payments and low utilization, asking to be added as an authorized user can boost your score by 20 to 40 points.

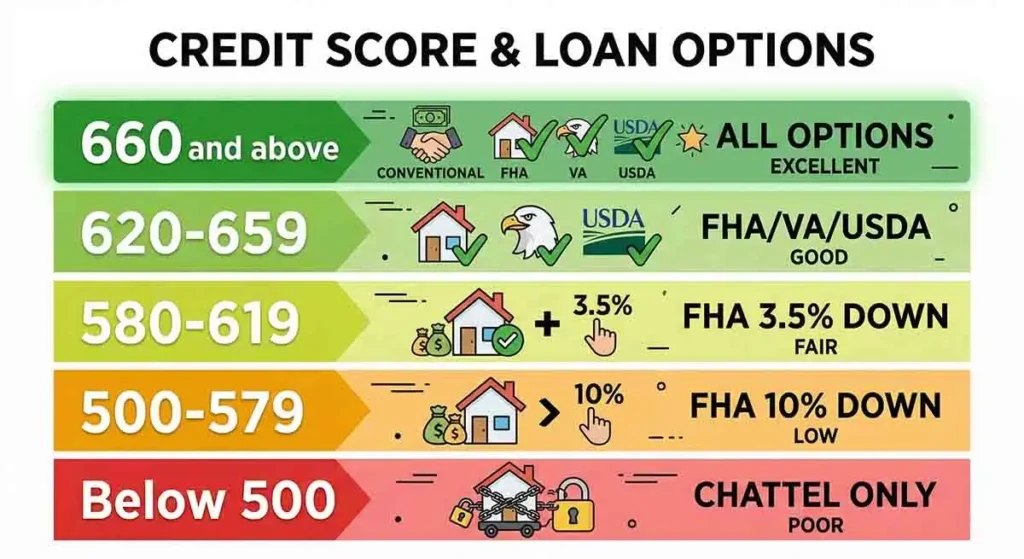

What to Expect with Different Credit Score Ranges

- Below 500: Very limited options. Focus on credit repair first before applying.

- 500 to 579: FHA with 10% down is your primary option. Work on improving to 580+ before applying.

- 580 to 619: FHA and chattel options open up meaningfully. 3.5% down becomes available for FHA.

- 620 to 659: Good range — FHA, VA (if eligible), USDA, and some conventional options available.

- 660 to 719: Excellent range — all programs available, good rates.

- 720+: Best available rates and terms across all programs.

The Bottom Line

The minimum credit score to buy a manufactured home depends on the loan type — as low as 500 for FHA with a large down payment, but 580 to 620 for most practical financing options. The higher your score, the better your rate and the more options you have.

If your score is not where it needs to be yet, do not give up. With focused effort on credit card balances and error disputes, most people can meaningfully improve their score within 3 to 6 months. A 50-point improvement in your credit score can translate to thousands of dollars in savings over the life of your loan.

Marcus T. Webb is a former bank loan officer with 14 years in manufactured home lending. He has originated FHA, VA, USDA, and chattel loans across North Carolina and Tennessee. Today he writes about manufactured home finance to help buyers avoid the costly mistakes he watched happen in banks for over a decade.