One of the most important protections a manufactured homeowner can have is the right insurance policy. But manufactured home insurance is not quite the same as standard homeowner’s insurance, and understanding what it covers and what it doesn’t can be the difference between recovering from a disaster and losing everything.

This guide explains exactly what manufactured home insurance covers, what is typically excluded, how much it costs, and how to choose the right policy for your specific situation.

What Is Manufactured Home Insurance?

Manufactured home insurance — sometimes called mobile home insurance — is a specialized form of property insurance designed specifically for factory-built homes. While it is similar in concept to a standard homeowner’s insurance policy, manufactured home insurance accounts for the unique structural characteristics, construction standards, and vulnerabilities of manufactured homes.

Not all standard homeowner’s insurance companies offer manufactured home coverage, and those that do often require a specialized rider or endorsement. Several insurers, including American Modern, Foremost, and American Family, specialize in or have dedicated programs for manufactured home insurance.

What Manufactured Home Insurance Typically Covers

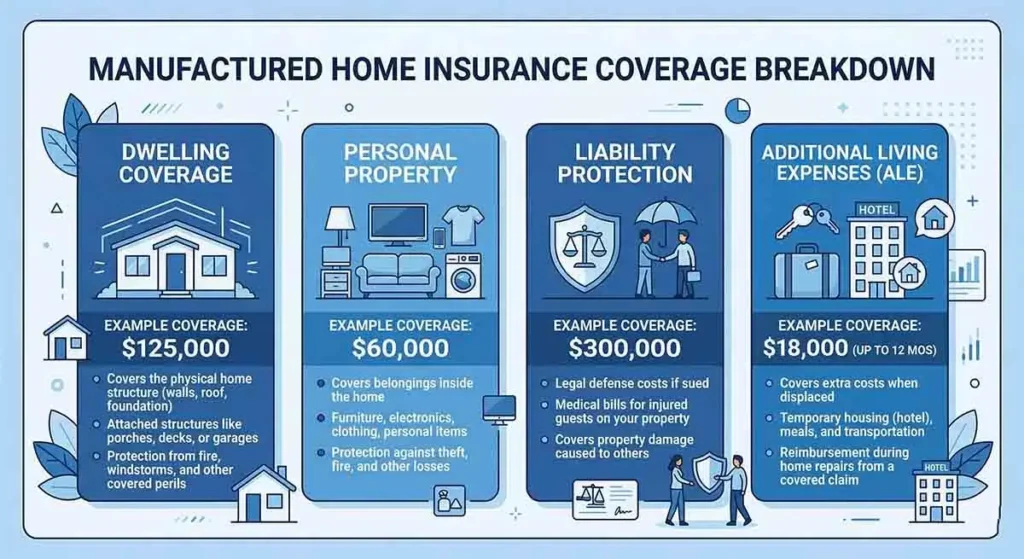

Dwelling Coverage (Coverage A)

Dwelling coverage is the core of any manufactured home policy. It covers the physical structure of your home — the walls, roof, floors, built-in appliances, plumbing, electrical systems, and heating and cooling systems — against covered perils.

Standard covered perils typically include:

- Fire and smoke damage

- Lightning strikes

- Windstorm and hail (with important exceptions — see below)

- Explosion

- Vandalism and malicious mischief

- Damage from vehicles or aircraft

- Frozen pipes (with conditions)

- Accidental discharge of water from plumbing

When purchasing dwelling coverage, you want coverage that is sufficient to rebuild your home at replacement cost, not just its current market value. Manufactured homes depreciate over time, and an actual cash value (ACV) policy will pay significantly less after depreciation is factored in. Always ask for replacement cost coverage if you can afford it.

Other Structures Coverage (Coverage B)

This covers detached structures on your property — a garage, carport, shed, fence, or deck — at typically 10% of your dwelling coverage limit. If you have a detached garage worth $15,000 and your dwelling coverage is $100,000, the standard 10% may not be enough. Ask your insurer about increasing this coverage if needed.

Personal Property Coverage (Coverage C)

Personal property coverage pays to repair or replace your belongings — furniture, clothing, electronics, appliances, and other items inside the home — if they are damaged or destroyed by a covered peril.

Standard personal property coverage limits vary, but a typical manufactured home policy might offer $20,000 to $50,000 in personal property coverage. As with dwelling coverage, ask whether this is on an ACV or replacement cost basis. Replacement cost personal property coverage costs more but pays significantly more in a claim.

Note that certain high-value items — jewelry, collectibles, firearms, musical instruments — may have sub-limits under a standard policy. If you own valuables, ask about scheduled personal property endorsements that provide higher, itemized coverage for specific items.

Liability Coverage (Coverage E)

Liability coverage protects you if someone is injured on your property or if you or a family member accidentally causes damage to someone else’s property. A standard manufactured home policy typically includes $100,000 in liability coverage, with options to increase to $300,000 or more.

Liability coverage is often the most undervalued part of a home insurance policy. If someone slips and falls on your steps and sues you for $200,000, your liability coverage is what stands between you and financial ruin.

Medical Payments Coverage (Coverage F)

This coverage pays medical bills for guests who are injured on your property, regardless of fault, up to a limit (typically $1,000 to $5,000). It is designed for minor incidents and helps prevent small injuries from escalating into liability claims.

Additional Living Expenses (ALE / Loss of Use)

If a covered loss makes your home uninhabitable, ALE coverage pays for temporary housing, meals, and other additional expenses while your home is being repaired. This is important coverage that is sometimes overlooked but can be critical if your home is severely damaged.

What Manufactured Home Insurance Does NOT Typically Cover

Understanding the exclusions in your policy is just as important as understanding what is covered. Common exclusions include:

Flood Damage

Standard manufactured home insurance does not cover flood damage — damage caused by rising water from outside the home, including storm surge, overflow of rivers or lakes, and surface water accumulation. Flood insurance must be purchased separately, typically through the National Flood Insurance Program (NFIP) or a private flood insurer.

This is critically important for manufactured homeowners. Manufactured homes are often placed in rural or low-lying areas that may be more susceptible to flooding. If your home is in a FEMA-designated flood zone, flood insurance may be required by your lender.

Earthquake Damage

Earthquakes are also excluded from standard manufactured home policies. If you live in an earthquake-prone area — California, the Pacific Northwest, parts of the Midwest — you may need to purchase a separate earthquake endorsement or policy.

Sinkhole Damage

Sinkhole coverage is excluded from most standard policies, though some states (particularly Florida) have special sinkhole coverage requirements. If you are in an area with sinkhole risk, ask your insurer specifically about this coverage.

Wear and Tear and Maintenance Issues

Insurance is designed to cover sudden, accidental losses — not gradual deterioration or deferred maintenance. Damage from rot, mold, pest infestation, or gradual water intrusion from a slow leak is typically excluded. This is why regular maintenance of your manufactured home is so important — insurance will not pay for problems that develop slowly over time.

Wind Damage in Some Coastal Areas

While wind damage is generally covered, some insurers exclude windstorm coverage in high-risk coastal areas (hurricane zones), or charge significantly higher premiums. In some parts of Florida, Texas, and the Gulf Coast, wind coverage must be purchased separately through a state-backed windpool program.

Vacant Home Damage

If your manufactured home is vacant for an extended period (typically 30 to 60 days, depending on the policy), coverage for certain perils may be reduced or eliminated. If you plan to leave your home unoccupied for an extended period, notify your insurer and ask about a vacancy endorsement.

Special Considerations for Park-Based Manufactured Homes

If your manufactured home is in a mobile home park, your insurance needs are somewhat different from homes on owned land:

- You typically do not need liability coverage for the land (the park carries that), but you do need it for incidents that originate in or around your home

- Some parks require a minimum amount of liability coverage as a condition of residency — check your lease

- If the park’s infrastructure (water lines, sewer, electrical pedestals) causes damage to your home, the park’s insurance may or may not cover it. Your policy’s other structures or dwelling coverage may apply

How Much Coverage Do You Need?

The right amount of coverage depends on:

- Dwelling coverage: Should equal the cost to rebuild your home at current construction costs. Get a replacement cost estimate from your insurer or a local builder. Many owners are significantly underinsured.

- Personal property: Take a home inventory. List your furniture, electronics, clothing, and other belongings and estimate their replacement value. Most people need at least $30,000 to $50,000 in personal property coverage.

- Liability: At minimum $100,000, but $300,000 is advisable if you have any significant assets to protect.

Top Insurance Companies for Manufactured Homes

Not every insurer covers manufactured homes. Companies with strong manufactured home programs include:

- Foremost Insurance: One of the largest and most specialized manufactured home insurers in the US

- American Modern: Specializes in specialty property insurance including manufactured homes

- American Family Insurance: Offers manufactured home coverage in many states

- Allstate: Offers manufactured home coverage through its specialty program

- GEICO: Partners with specialty insurers to offer manufactured home policies

Always get at least three quotes before purchasing. Manufactured home insurance premiums vary significantly between insurers for the same coverage, and shopping around can save you $300 to $700 per year.

How to Save Money on Manufactured Home Insurance

- Bundle with auto insurance: Most insurers offer 5 to 15 percent discounts for bundling

- Install smoke and carbon monoxide detectors: Safety features often earn discounts

- Install a security system: Many insurers offer discounts for monitored alarm systems

- Choose a higher deductible: Raising your deductible from $500 to $1,000 can reduce premiums by 10 to 15 percent

- Maintain a claims-free record: Avoid filing small claims that can raise your premium or result in non-renewal

- Tie-down and anchor your home: Properly anchored homes are less vulnerable to wind damage and may qualify for lower premiums

The Bottom Line

Manufactured home insurance is not optional — it is essential protection for what is likely your most valuable asset. The right policy covers your home’s structure, your belongings, your liability, and your living expenses if disaster strikes.

Read your policy carefully, understand the exclusions, and make sure your dwelling coverage is sufficient to actually rebuild your home if it is totally destroyed. And never assume flood or earthquake coverage is included — it almost never is.

Marcus T. Webb is a former bank loan officer with 14 years in manufactured home lending. He has originated FHA, VA, USDA, and chattel loans across North Carolina and Tennessee. Today he writes about manufactured home finance to help buyers avoid the costly mistakes he watched happen in banks for over a decade.