Walk into any conversation about factory-built homes and you will quickly run into confusion about manufactured homes vs. modular homes. Many people use these terms interchangeably, but they are actually two very different types of housing — different in how they are built, what codes they follow, how they are financed, and how they are treated legally.

Understanding the difference matters enormously if you are trying to buy one. This guide gives you the clearest, most complete comparison available.

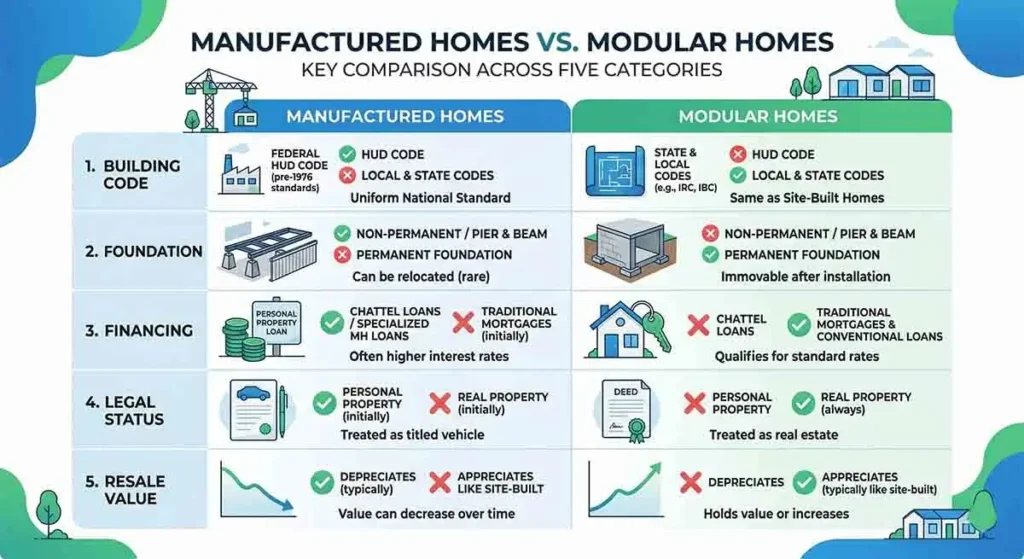

The Single Most Important Difference: Which Building Code

The defining legal difference between a manufactured home and a modular home is which building code governs its construction.

Manufactured homes are built to the HUD Code — a federal building standard set by the U.S. Department of Housing and Urban Development. Every manufactured home built in the United States after June 15, 1976 must comply with this code, and each home receives a red certification label (the HUD tag) attached to each section.

Modular homes are built to local and state building codes — the same codes that govern site-built homes in a given state or county. Because these codes vary by location, a modular home built for installation in Texas is built differently from one built for Vermont.

How Each Type Is Built

How Manufactured Homes Are Built

Manufactured homes are built entirely in a factory on a permanent steel chassis. The steel undercarriage is a structural part of the home — it supports the floor and enables transportation. Sections are built, fitted with insulation, wiring, plumbing, and interior finishes, then transported to the building site on wheels using the home’s own chassis.

How Modular Homes Are Built

Modular homes are also built in a factory in sections, but they are built on temporary frames rather than a permanent steel chassis. The sections are transported to the site on truck flatbeds, lifted by crane onto a permanent foundation, joined together, and the temporary transport frames are removed.

Foundation Differences

Manufactured homes can technically be placed on either permanent or non-permanent foundations. When placed non-permanently (on piers, blocks, or in a mobile home park), the home retains its personal property status.

Modular homes are always placed on permanent foundations. There is no option for a modular home to be set up non-permanently, because it does not have its own chassis.

Legal Classification: Personal Property vs. Real Property

A manufactured home placed on leased land is personal property — like a vehicle. A manufactured home on owned land with a permanent foundation can be converted to real property, but this requires an active conversion process.

A modular home, once assembled on a permanent foundation, is automatically real property — the same legal status as a site-built home. No conversion process is needed.

Financing Comparison

Manufactured Home Financing

- In a park on leased land: Chattel loans (high interest, short terms)

- On owned land with permanent foundation: FHA, VA, USDA, or conventional mortgage

- Without HUD tags or pre-1976: Very difficult to finance

Modular Home Financing

- Modular homes are financed like site-built homes from day one

- Conventional mortgages, FHA, VA, USDA — all standard mortgage programs apply

- Interest rates and terms are the same as for site-built homes

- Construction loans are available during the building phase

Cost Comparison

Purchase Price (2026 Estimates)

- Manufactured homes (new double wide): $90,000 to $200,000

- Modular homes (new): $150,000 to $350,000+

Manufactured homes are generally less expensive because they use different materials, are built to the federal HUD Code rather than more stringent local codes, and benefit from greater economies of scale in factory production.

Resale Value and Appreciation

Historically, modular homes have appreciated more reliably than manufactured homes because they are treated as real estate from day one and are built to local building codes. Appraisers value them similarly to site-built homes.

Manufactured homes on owned land with permanent foundations have improved significantly in their appreciation track record, particularly in the last decade. However, manufactured homes in parks or without permanent foundations still tend to depreciate.

Quality and Durability

Modern manufactured homes — particularly those built in the last 10 to 15 years — are substantially better built than those of the 1970s and 1980s. Today’s HUD Code manufactured homes must meet standards for structural strength, energy efficiency, wind resistance, and fire safety that are genuinely rigorous.

Modular homes, built to local codes, are generally somewhat more similar to site-built homes in materials and construction methods. But the quality gap between manufactured and modular homes is much smaller today than it was a generation ago.

Which Is Right for You?

Choose a manufactured home if:

- Budget is your primary concern and you need the lowest possible purchase price

- You are buying a home for a park or rural location

- You plan to own land and convert to real property

Choose a modular home if:

- You want the financing simplicity and resale value of a site-built home

- You are building on land you own and want the home treated as real estate immediately

- Your local zoning restricts manufactured homes but allows modular construction

- You have a higher budget and want materials closer to site-built quality

The Bottom Line

Manufactured homes and modular homes are not the same thing, and treating them as interchangeable will lead to costly mistakes with financing, insurance, and legal planning. Know which type you are buying, understand the code it was built to, and plan your land ownership and foundation strategy accordingly.

Both types of factory-built housing offer excellent value compared to traditional site-built construction — when you go in with the right information.

Rafael Medina is a two-time manufactured home buyer who went from a 611 credit score and $8,000 savings to owning two manufactured homes — one in a park and one on private land with an FHA mortgage. He writes for first-time buyers and park residents, covering the practical, real-world side of manufactured home ownership from someone who has lived every step of it.