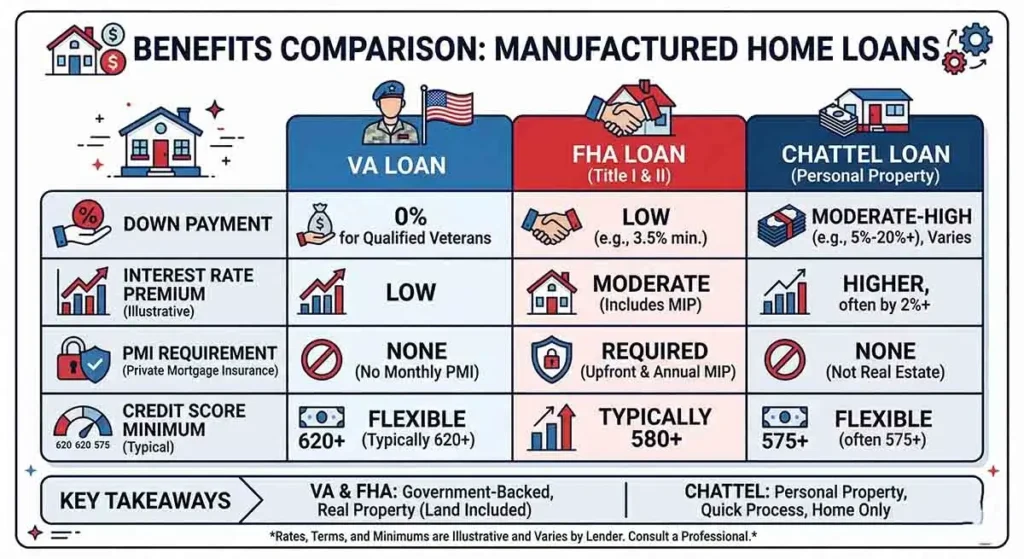

For eligible veterans, service members, and surviving spouses, a VA loan for a manufactured home is one of the most powerful financing tools available. VA loans come with no down payment requirement, no private mortgage insurance, and competitive interest rates — benefits that can save tens of thousands of dollars over the life of a loan compared to other manufactured home financing options.

But VA loans for manufactured homes come with specific requirements that not all manufactured homes and not all situations qualify for. This complete guide explains everything veterans need to know.

What Is a VA Loan?

A VA loan is a mortgage loan guaranteed by the U.S. Department of Veterans Affairs (VA). The VA does not make the loans directly — you apply through a VA-approved private lender — but the VA guarantees a portion of the loan, which allows lenders to offer favorable terms to eligible borrowers.

VA loans are available to veterans who have served a minimum active duty period, active-duty service members, National Guard and Reserve members who meet certain service requirements, and surviving spouses of veterans who died in service or from a service-connected disability.

Key Benefits of VA Loans for Manufactured Homes

- No down payment required: Eligible borrowers can finance 100% of the purchase price with no down payment

- No private mortgage insurance (PMI): Unlike FHA and conventional loans with less than 20% down, VA loans do not require PMI, saving hundreds of dollars per month

- Competitive interest rates: VA loan rates are typically 0.25 to 0.5 percentage points below conventional loan rates

- Limited closing costs: The VA limits the fees lenders can charge veterans

- No prepayment penalty: You can pay off the loan early without penalty

- Assumable loan: VA loans can be assumed by another buyer when you sell, which is valuable when rates are rising

VA Loan Requirements for Manufactured Homes

The VA has specific requirements that manufactured homes must meet to be eligible for VA financing. These requirements are stricter than what some other loan programs require, and it is important to understand them before selecting a home.

The Home Must Be on a Permanent Foundation

This is the most important requirement. The VA will only finance a manufactured home that is permanently affixed to land — meaning it is on a permanent foundation that meets VA and HUD standards. The home cannot be in a mobile home park on leased land. The borrower must own the land or be purchasing it as part of the same transaction.

The Home Must Be Titled as Real Property

The manufactured home must be classified as real estate — not personal property. If the home still has a personal property (vehicle-type) title, it must be converted to a real property deed before the VA loan can close.

HUD Compliance

The home must have been built on or after June 15, 1976, meeting HUD Manufactured Home Construction and Safety Standards. The home must display HUD certification labels (red tags). Homes built before this date — technically mobile homes — do not qualify for VA financing.

Minimum Size

The VA requires that manufactured homes have a minimum floor area of 400 square feet. In practice, most manufactured homes meet this requirement easily, but very small single wides or specialty homes may not.

Primary Residence Only

VA loans are for primary residences only. You cannot use a VA loan to finance a manufactured home as a vacation property, second home, or investment/rental property.

No Wheels, Axles, or Hitch

By the time of closing, the transportation undercarriage — wheels, axles, and hitch — must have been removed from the home, confirming its permanent placement.

Foundation Certification

A licensed engineer must certify that the manufactured home’s foundation meets HUD’s Permanent Foundations Guide for Manufactured Housing. This certification is typically required during the appraisal process and costs $300 to $600.

VA Loan Entitlement and Manufactured Homes

VA loan entitlement works the same way for manufactured homes as for site-built homes. If you have your full entitlement available (never used a VA loan, or paid off a previous VA loan), you can typically borrow without a down payment up to conforming loan limits in your area.

Veterans with remaining entitlement from a previous VA loan can still use it for a manufactured home purchase, though they may need a down payment if the purchase price exceeds their available entitlement.

The VA Funding Fee

One cost unique to VA loans is the VA funding fee — a one-time charge that helps fund the VA loan program for future veterans. For manufactured home purchases in 2026:

- First-time VA loan use: 2.15% of the loan amount (0% down)

- Subsequent use: 3.3% of the loan amount (0% down)

- With down payment (5% or more): 1.5% of the loan amount

- With down payment (10% or more): 1.25% of the loan amount

The funding fee can be financed into the loan rather than paid at closing. Veterans with a service-connected disability rating of 10% or more are exempt from the VA funding fee entirely — a significant benefit.

Credit Score Requirements for VA Manufactured Home Loans

The VA itself does not set a minimum credit score. However, lenders who make VA loans set their own minimum scores, which typically range from 580 to 620. For manufactured home VA loans specifically, some lenders require 620 or higher because manufactured home collateral is considered slightly higher risk.

In practice, a credit score of 640 or above will give you access to the widest range of VA manufactured home lenders and the most competitive rates.

Finding VA Lenders Who Finance Manufactured Homes

This is where many veterans run into difficulty. Not every VA-approved lender offers manufactured home loans, and some lenders who technically offer them have limited experience with the unique requirements of manufactured home VA transactions.

Look specifically for lenders who advertise VA manufactured home loans on their websites and who have loan officers experienced with the manufactured home VA loan process. The VA’s lender locator at benefits.va.gov/homeloans can help you find approved lenders, but you will need to ask each one specifically about their manufactured home VA loan experience.

Some lenders that have historically been active in VA manufactured home lending include Veterans United Home Loans, Caliber Home Loans, and several regional banks and credit unions in states with high manufactured home concentrations like Texas, North Carolina, and Florida.

The VA Manufactured Home Loan Process

- Get your Certificate of Eligibility (COE): Apply through the VA’s eBenefits portal or ask your lender to pull it for you. The COE confirms your eligibility for VA benefits.

- Check your credit and finances: Review your credit report, calculate your DTI, and make sure your finances are in order before applying.

- Find a VA-experienced lender: Interview at least two or three lenders with specific manufactured home VA experience.

- Get pre-approved: This gives you a clear budget and shows sellers you are a serious buyer.

- Find your home and lot: Remember, the home must be (or will be placed on) land you own, on a permanent foundation.

- VA appraisal: A VA-assigned appraiser will assess the home’s value and confirm it meets VA requirements. The foundation certification happens here.

- Underwriting and closing: Once the appraisal is complete and all conditions are met, underwriting is completed and you close on the loan.

What If the Home Does Not Currently Meet VA Requirements?

If you find a manufactured home you love but it does not currently meet VA requirements — for example, it is in a park, or it does not yet have a permanent foundation — you have options:

- Move the home to land you own, install a permanent foundation, and convert the title to real property before applying for the VA loan

- Use a construction or renovation loan to add the required permanent foundation before converting to VA financing

- Use another loan type (FHA chattel, for example) as a bridge while you work toward meeting VA requirements

The Bottom Line

A VA loan for a manufactured home is one of the best financing deals available in the entire US housing market — no down payment, no PMI, and competitive rates. But the requirements are real: the home must be on a permanent foundation on land you own, titled as real property, and meet HUD standards.

For eligible veterans who can meet these requirements, a VA manufactured home loan is absolutely worth pursuing. The lifetime savings compared to a chattel loan or even an FHA loan can be substantial — often $50,000 to $100,000 or more over the life of the loan.

Marcus T. Webb is a former bank loan officer with 14 years in manufactured home lending. He has originated FHA, VA, USDA, and chattel loans across North Carolina and Tennessee. Today he writes about manufactured home finance to help buyers avoid the costly mistakes he watched happen in banks for over a decade.