If you are budgeting for a manufactured home purchase, one of the biggest practical questions is: how much does manufactured home insurance cost? The answer ranges more widely than most buyers expect — from as low as $300 per year to over $2,000 per year — and understanding what drives those differences can help you shop smarter and pay less.

This guide covers average premiums, the specific factors that affect your rate, the top insurance companies for manufactured homes, and practical tips to lower your premium.

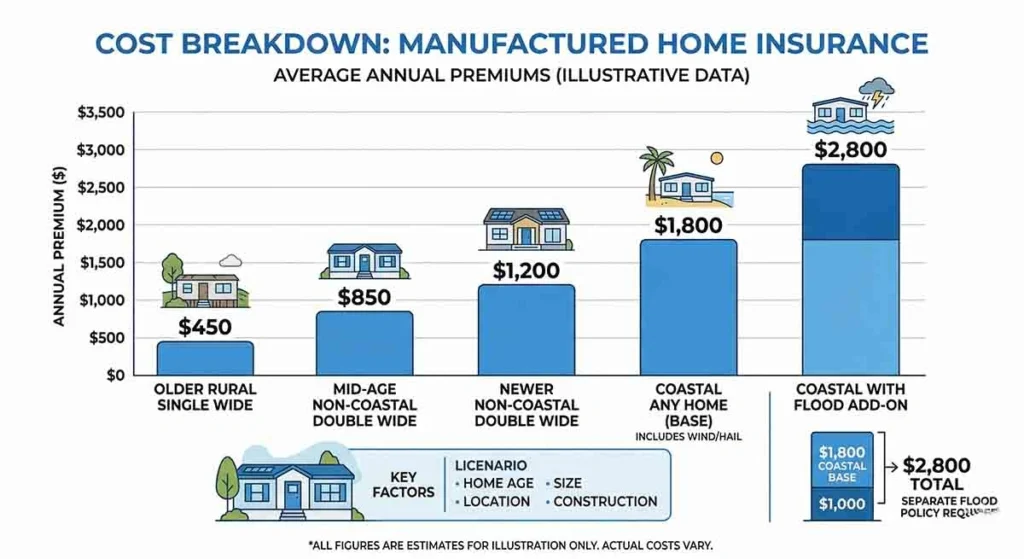

Average Manufactured Home Insurance Cost in 2026

The national average cost of manufactured home insurance in 2026 is approximately $800 to $1,200 per year — or $67 to $100 per month. However, this average masks enormous variation based on location, home value, coverage level, and other factors.

Here is a realistic range by coverage level and home type:

- Older single wide, basic coverage, rural area: $300 to $600 per year

- Mid-age double wide, standard coverage, non-coastal: $700 to $1,100 per year

- Newer double wide, full replacement cost, non-coastal: $1,000 to $1,600 per year

- Any manufactured home, coastal or hurricane zone: $1,500 to $3,000+ per year

For comparison, the average standard homeowner’s insurance policy for a site-built home in the US costs approximately $1,400 per year. Manufactured home insurance is typically less expensive than site-built homeowner’s insurance because manufactured homes have lower replacement costs — though the gap narrows when comparing similar coverage levels and values.

What Factors Affect Your Manufactured Home Insurance Premium?

Location — The Biggest Factor

Where your home is located accounts for more variation in manufactured home insurance premiums than any other single factor. Location affects the risk of:

- Hurricanes and wind: Homes in coastal Florida, Texas Gulf Coast, the Carolinas, and other hurricane-prone areas pay dramatically higher premiums for wind coverage — or must purchase separate windstorm coverage from a state plan

- Tornadoes: Homes in tornado alley (Oklahoma, Kansas, Nebraska, Missouri, parts of Texas and the Southeast) pay higher wind premiums

- Wildfires: Homes in fire-prone Western states face higher wildfire risk premiums

- Severe winter weather: Homes in areas with heavy snow loads or severe freeze risk may face higher premiums

Home Age and Value

Newer manufactured homes cost more to insure because they cost more to replace. Homes built in the last 10 years with modern materials and construction are more expensive to rebuild than older homes. However, newer homes may also qualify for discounts because of their better construction standards and improved safety features.

Older manufactured homes — particularly those built before 1976 — can be difficult and expensive to insure, and some insurers will not cover them at all.

Coverage Type: ACV vs. Replacement Cost

This is one of the most important decisions you will make when buying manufactured home insurance:

- Actual Cash Value (ACV) coverage pays out what your home is currently worth at the time of a loss, accounting for depreciation. ACV policies are cheaper but pay out significantly less in a claim — a 20-year-old home that cost $80,000 new might only be worth $30,000 at ACV, which is what the insurance pays to rebuild it (which actually costs much more than that).

- Replacement Cost coverage pays to rebuild or replace your home at current costs, regardless of its depreciated value. This type costs more per year but provides dramatically better financial protection after a total loss.

Whenever financially possible, choose replacement cost coverage. The premium difference is typically $100 to $300 per year, but the difference in payout after a total loss can be tens of thousands of dollars.

Coverage Amounts

Higher dwelling coverage limits, higher personal property limits, and higher liability limits all increase premiums. Matching your coverage closely to actual needs — without over-insuring or under-insuring — optimizes your premium-to-protection ratio.

Deductible Amount

Your deductible is the amount you pay out of pocket before insurance kicks in for a claim. Higher deductibles mean lower premiums:

- $500 deductible vs. $1,000 deductible: Typically saves 10 to 15% on premium

- $1,000 deductible vs. $2,500 deductible: Typically saves an additional 10 to 20%

Raise your deductible to the highest level you can comfortably cover from savings. This is one of the most reliable ways to reduce your premium without reducing your actual coverage level for serious losses.

Claims History

If you have filed claims in the past — particularly multiple claims within a few years — your premium will be higher. Insurers view a history of claims as a predictor of future claims. Avoiding small claims that you could pay out of pocket helps keep your premium lower over time.

Credit Score (In Most States)

Most manufactured home insurance companies use credit-based insurance scores when setting premiums. Higher credit scores typically result in lower insurance premiums. This is one more reason to maintain good credit — it affects not just your loan rate but also your insurance costs.

Safety Features and Construction

Manufactured homes with certain safety features may qualify for premium discounts:

- Smoke detectors and carbon monoxide detectors

- Monitored security and fire alarm systems

- Proper tie-down and anchoring systems (reduces wind damage risk)

- Storm shutters or impact-resistant windows in hurricane zones

- Newer electrical systems (older wiring types like aluminum wiring can increase premiums)

Top Insurance Companies for Manufactured Homes in 2026

Foremost Insurance Group

Foremost is the largest specialized manufactured home insurer in the United States, with decades of experience and policies available in all 50 states. They offer both ACV and replacement cost options, and their claims handling for manufactured home losses is generally well-regarded. Foremost is a good first quote to get.

American Modern Insurance Group

American Modern specializes in specialty property insurance including manufactured homes, RVs, and other non-standard properties. They offer competitive rates, particularly for older homes that other insurers may decline. Their coverage options are comprehensive.

American Family Insurance

American Family offers manufactured home coverage in many states, with the added benefit of strong bundling discounts with auto insurance. If you are already an American Family auto customer, getting a manufactured home quote from them is worthwhile.

Allstate (through their Specialty Manufactured Home program)

Allstate offers manufactured home coverage through a specialty program in most states. Their brand name and financial stability are positives, and they offer competitive bundling discounts.

State Farm

State Farm offers manufactured home coverage in many states, with competitive rates for newer homes. Their agent network and local presence can be an advantage for claims service.

How to Get the Best Price on Manufactured Home Insurance

- Get at least three quotes: Premium differences of 30 to 50% between insurers for identical coverage are common. Shop around every year at renewal.

- Bundle with auto insurance: Bundling typically saves 5 to 20% on the manufactured home policy and often on the auto policy as well.

- Raise your deductible: As discussed above, this is one of the most reliable ways to reduce your premium.

- Improve your credit score: Over time, a better credit score translates to lower premiums in most states.

- Install safety features: Smoke detectors, monitored alarms, and proper tie-downs can earn meaningful discounts.

- Avoid small claims: File only significant claims. Paying for minor repairs out of pocket preserves your claims-free discount.

- Ask about discounts specifically: Some discounts (senior discounts, long-term customer discounts, paid-in-full discounts) are not always automatically applied — ask for them.

What About Flood Insurance?

Standard manufactured home insurance does not cover flood damage — water rising from outside the home due to storms, overflowing rivers, or other external water events. If your manufactured home is in or near a flood zone, you need separate flood insurance.

Flood insurance is available through the National Flood Insurance Program (NFIP) or through a growing number of private flood insurers. NFIP premiums for manufactured homes average $500 to $2,000 per year depending on flood zone designation and coverage amount. If you are in a high-risk flood zone (Zone AE or V), flood insurance may be required by your lender.

The Bottom Line

Manufactured home insurance in 2026 costs $300 to $3,000+ per year depending on your location, home age and value, coverage level, and deductible. The single best thing you can do is get multiple quotes — premium variation between insurers is significant — and make sure you have replacement cost coverage rather than ACV coverage.

Do not let the cost of insurance be a surprise. Budget for it upfront as part of your total monthly housing cost, and review your coverage and shop for better rates every year at renewal.

Marcus T. Webb is a former bank loan officer with 14 years in manufactured home lending. He has originated FHA, VA, USDA, and chattel loans across North Carolina and Tennessee. Today he writes about manufactured home finance to help buyers avoid the costly mistakes he watched happen in banks for over a decade.