The fight for affordable housing has given rise to two prominent alternatives to traditional homeownership: the manufactured home and the tiny house. Both are marketed as affordable, practical housing solutions — but they are very different in reality. In this guide, we compare manufactured homes vs. tiny houses across every dimension that matters to a buyer in 2026.

What We Mean by Each Term

Before comparing them, let us define what we are talking about:

Manufactured homes (our focus at ownednotowned.com/) are factory-built homes constructed to the federal HUD Code. They typically range from 600 square feet (single wide) to 2,500+ square feet (double wide or triple wide) and are designed to be placed on a semi-permanent or permanent foundation. They are regulated at the federal level, financeable through multiple loan programs, and occupied by over 22 million Americans.

Tiny houses are a broad category that includes tiny houses on wheels (THOWs), tiny houses on foundations, and park model RVs. The “tiny house movement” celebrates homes under approximately 400 square feet. Tiny houses on wheels are built on trailer chassis, while tiny houses on foundations are essentially very small site-built or modular homes.

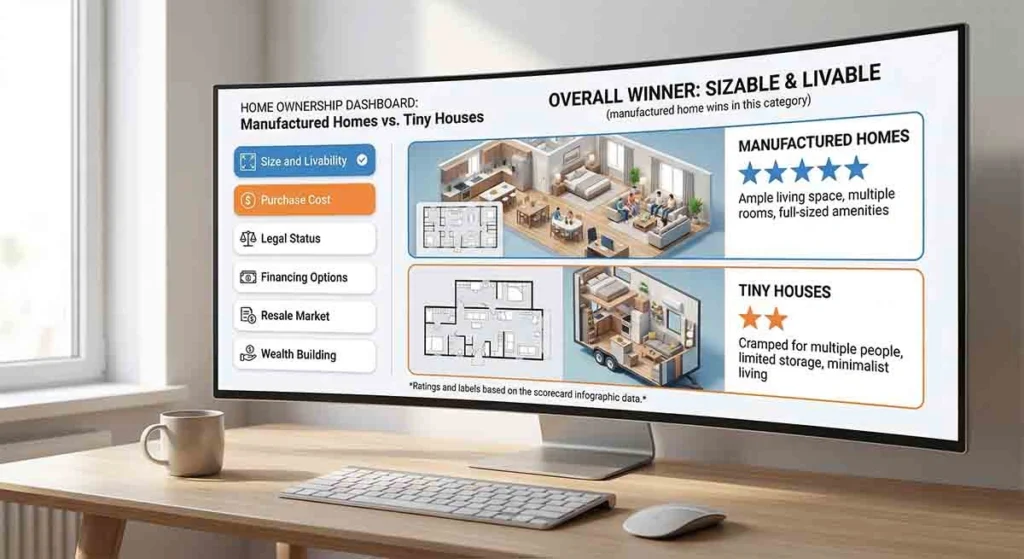

Size and Livability

This is the most fundamental difference. A typical tiny house is 100 to 400 square feet. A typical manufactured home — even a modest single wide — is 700 to 1,200 square feet. A double wide is 1,400 to 2,400 square feet.

The livability implications are enormous. A tiny house works best for single individuals or couples without children who embrace a minimalist lifestyle. It typically has a lofted sleeping area accessed by steep stairs or a ladder, very limited storage, and a small kitchen and bathroom that require constant organization to function.

A manufactured home, even a modest single wide, has full-sized rooms, standard-height ceilings, real closets, a full kitchen, and a bathroom or two that feel like a normal home. Families with children, people with mobility challenges, people who work from home, or anyone who is not committed to an extreme minimalist lifestyle will find a manufactured home dramatically more livable than a tiny house.

Cost Comparison

Purchase Price

Tiny houses have a wide price range depending on whether they are DIY-built, purchased from a builder, or on a foundation:

- DIY tiny house on wheels: $20,000 to $60,000

- Custom-built tiny house on wheels: $60,000 to $150,000

- Tiny house on foundation (very small): $100,000 to $200,000+

Manufactured homes:

- New single wide: $50,000 to $110,000

- New double wide: $90,000 to $200,000

- Used single or double wide: $15,000 to $100,000

The purchase prices overlap in many ranges, but when you consider what you get for the money — livable square footage — manufactured homes almost always deliver more value per dollar.

Total Cost to Occupy

Both home types require land (or a place to park or hook up). A tiny house on wheels requires a hookup location — which might be a tiny house community, a friend’s property, or an RV park. A manufactured home requires a lot (owned or leased). When you factor in the total cost of both the home and a place to put it legally and comfortably, the costs tend to converge significantly.

Legal and Zoning Issues

This is where tiny houses face a much harder challenge than manufactured homes.

Manufactured Home Zoning

Manufactured homes built to HUD Code have legal recognition under federal law. While local zoning restrictions can and do affect where manufactured homes can be placed, they have a legal framework that protects them in many jurisdictions. Zoning for manufactured homes, while not uniformly accommodating, is much clearer than for tiny houses.

Tiny House Zoning

Tiny houses — particularly those on wheels — face an extremely difficult legal and regulatory environment in most of the United States. In the vast majority of jurisdictions:

- A tiny house on wheels is legally classified as an RV, not a dwelling

- Most residential zones prohibit permanent residence in an RV

- Parking a THOW on private property and living in it full-time is illegal in many localities

- Even areas that have created tiny house ordinances typically have very limited sites available

The practical reality is that many tiny house owners live in legal gray areas — on friends’ properties, in RV parks that technically prohibit full-time residence, or in communities that look the other way. This creates genuine legal vulnerability that manufactured home owners do not face.

Financing

Financing is another area where manufactured homes have a substantial structural advantage.

Manufactured homes can be financed through FHA loans, VA loans, USDA loans, conventional mortgages (Fannie Mae MH Advantage), and chattel loans. A buyer with reasonable credit and a small down payment has genuine, accessible financing options.

Tiny houses on wheels cannot be financed with traditional mortgages because they are classified as RVs or personal property. Financing options include:

- RV loans (typically higher rates than mortgages, shorter terms)

- Personal loans (even higher rates, unsecured)

- Credit cards (avoid for large purchases)

- Cash or builder financing

Tiny houses on foundations can potentially be financed with mortgages, but lenders often struggle to appraise homes under 400 square feet because there are no comparable sales. This makes financing difficult and sometimes impossible.

Resale Value

Manufactured homes on owned land have a recognized, active resale market. They are listed on the MLS, sold through real estate agents, and appraised using standard methods. While the market is smaller than site-built homes, it is genuine and functional.

Tiny houses — particularly those on wheels — have a much more limited and less liquid resale market. THOWs depreciate rapidly (they are legally RVs, and RVs depreciate). The market of potential buyers is smaller, less organized, and largely online through niche platforms. Selling a tiny house for anything close to its original cost is difficult in most markets.

Long-Term Financial Building

Manufactured homes on owned land build equity and can appreciate in value over time. They can be refinanced to access equity. They contribute to the owner’s net worth in a measurable, bankable way.

Tiny houses on wheels are more similar to a vehicle or RV in their financial profile — they are depreciating assets that do not typically contribute to long-term wealth building in the way real estate does.

Which Is Actually Better for Most People?

Based on the complete comparison, manufactured homes win on virtually every practical dimension for most buyers:

- More livable space per dollar

- Clearer legal standing and zoning recognition

- Accessible mortgage-type financing

- Active resale market

- Potential for appreciation and equity building

Tiny houses make sense for a specific type of buyer: someone genuinely committed to an extreme minimalist lifestyle, comfortable with legal ambiguity in many areas, able to pay cash or accept high-cost financing, and not primarily focused on long-term wealth building through real estate.

For anyone who wants an affordable home that functions like a real home, builds equity, and exists within a clear legal framework — a manufactured home is the better choice in 2026.

The Bottom Line

The tiny house movement is inspiring and has genuine appeal for a subset of Americans. But for most buyers seeking affordable homeownership in 2026, a manufactured home delivers more livability, better legal standing, more accessible financing, and stronger long-term financial potential than a tiny house.

Rafael Medina is a two-time manufactured home buyer who went from a 611 credit score and $8,000 savings to owning two manufactured homes — one in a park and one on private land with an FHA mortgage. He writes for first-time buyers and park residents, covering the practical, real-world side of manufactured home ownership from someone who has lived every step of it.