One of the most common questions from people exploring manufactured home ownership is: can you get a mortgage on a manufactured home? The answer — the real, complete answer — is yes, but only under specific conditions that not every manufactured home or every buyer situation meets.

Understanding exactly when a mortgage is available and when it is not will help you plan your purchase strategy correctly from the start and avoid one of the most expensive mistakes in manufactured home buying.

The Short Answer

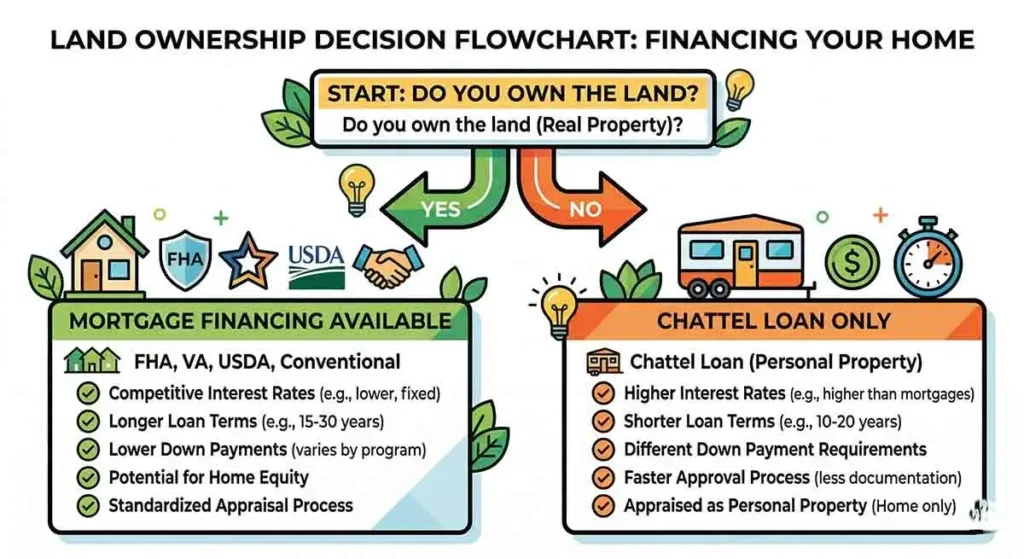

Yes, you can get a mortgage on a manufactured home — a real, traditional mortgage with 30-year terms and mortgage-level interest rates — but the home must be real property, not personal property. That single requirement shapes everything else.

Real Property vs. Personal Property: Why It Determines Everything

In US law, a manufactured home can be classified either as personal property (like a vehicle) or as real property (like a house). The classification depends on two things:

- Whether you own the land the home sits on

- Whether the home is permanently affixed to that land on a qualifying foundation

When both conditions are met — you own the land and the home is on a permanent foundation — the home can be (or already is) classified as real property, and mortgage financing becomes available. When either condition is absent — the land is leased or the home is not on a permanent foundation — the home is personal property, and you are limited to chattel financing (personal property loans), which is significantly more expensive.

What Types of Mortgages Are Available for Manufactured Homes?

FHA Title II Loans

FHA Title II loans are the most commonly used mortgage product for manufactured homes in the United States. These are full mortgages insured by the Federal Housing Administration, available with:

- Down payments as low as 3.5 percent (with 580+ credit score)

- 30-year fixed terms

- Competitive interest rates (typically 0.5 to 1 percentage point above conventional mortgage rates)

- Available to borrowers with credit scores as low as 580

Requirements: Home must be on owned land, on a permanent foundation, titled as real property, and meet all HUD compliance standards.

VA Loans

VA loans for manufactured homes offer the most favorable terms available — zero down payment, no private mortgage insurance, and competitive rates — for eligible veterans, active-duty service members, and qualifying surviving spouses. The home must be on owned land with a permanent foundation and must be titled as real property.

USDA Rural Development Loans

USDA loans provide zero-down-payment financing for manufactured homes in USDA-eligible rural areas. Income limits apply (typically up to 115% of area median income), and the home must be on owned land with a permanent foundation in a qualifying rural area.

Conventional Loans (Fannie Mae MH Advantage and Freddie Mac CHOICEHome)

Both Fannie Mae and Freddie Mac have programs that allow conventional mortgage financing for manufactured homes that meet specific design and construction standards. The MH Advantage and CHOICEHome programs require homes with:

- Site-built-like features — pitched roofs of specific slope, covered porch or entry, garages or carports, drywall interiors

- Permanent foundations on owned land

- Real property title

These programs offer rates closer to traditional site-built home mortgage rates and lower MIP requirements than FHA loans for qualified homes and borrowers.

When You Cannot Get a Mortgage: Chattel Loan Territory

You cannot get a traditional mortgage when:

The Home Is in a Mobile Home Park on Leased Land

Without land ownership, there is no real property to mortgage. You are limited to chattel loans — personal property loans that function like vehicle financing. Chattel loan characteristics:

- Interest rates typically 2 to 5 percentage points above mortgage rates

- Loan terms of 15 to 25 years rather than 30 years

- Higher monthly payments for the same loan balance

- No land equity building

The Home Does Not Have a Permanent Foundation

Even on owned land, a home without a permanent foundation qualifying under HUD’s Permanent Foundations Guide cannot be mortgaged. The foundation must be concrete — pier-and-beam, perimeter, or engineered slab — not temporary piers, blocking, or stacking.

The Home Is Not Yet Titled as Real Property

Even if the home is on owned land with a permanent foundation, the mortgage cannot close until the personal property title has been surrendered and the home has been recorded as part of the real estate deed. This conversion process — retiring the title — must be completed before mortgage financing can proceed.

The Home Was Built Before June 15, 1976

Pre-HUD Code homes — technically mobile homes — cannot be financed with FHA, VA, or USDA mortgages. Some conventional lenders will not finance them either. Very old homes may only qualify for chattel loans with specialty lenders, at higher rates and stricter terms.

The Interest Rate Difference: Why Getting a Mortgage Matters So Much

The difference between chattel financing and mortgage financing is not academic — it directly affects how much you pay every month and over the life of the loan. Consider this comparison:

$120,000 chattel loan at 10% interest over 20 years: Monthly payment — approximately $1,158. Total interest paid — approximately $157,920.

$120,000 FHA mortgage at 7% interest over 30 years: Monthly payment — approximately $799. Total interest paid — approximately $167,640.

While the total interest over 30 years is similar in this example, the monthly payment difference of $359 is very significant for household budgets. And VA Loans and USDA loans at even lower rates save substantially more. Additionally, the 30-year term means each mortgage payment builds more equity faster through principal reduction than the 20-year chattel loan at higher principal amounts per payment.

How to Position Yourself to Get a Mortgage

If mortgage financing is your goal — and it should be for most buyers — here is the path:

- Buy land. Land ownership is non-negotiable for mortgage financing. If you cannot buy land now, start planning and saving for it.

- Install a permanent foundation. Budget for a qualifying permanent foundation as part of your project cost. A perimeter concrete foundation typically costs $4,000 to $12,000 depending on home size and local labor.

- Convert the title to real property. Complete the affidavit of affixture process and record the home as part of the real estate deed. This process is detailed in our separate conversion guide.

- Work with a lender experienced in manufactured home mortgages. Not every mortgage lender handles manufactured home loans. Find a lender with specific experience in FHA Title II, VA, or USDA manufactured home financing.

- Prepare your finances. Minimum credit score of 580 for FHA (620 preferred), documented income, manageable debt-to-income ratio.

The Bottom Line

You can absolutely get a mortgage on a manufactured home — but only if the home is on land you own, on a permanent foundation, and titled as real property. Meeting these three conditions unlocks access to FHA, VA, USDA, and conventional mortgage programs with dramatically better terms than chattel financing.

If you are buying a manufactured home and long-term financial health is a priority, structure your purchase to meet these mortgage requirements from day one. The difference in monthly payments, total interest, and equity building over a 20-to-30-year period is tens of thousands of dollars.

Marcus T. Webb is a former bank loan officer with 14 years in manufactured home lending. He has originated FHA, VA, USDA, and chattel loans across North Carolina and Tennessee. Today he writes about manufactured home finance to help buyers avoid the costly mistakes he watched happen in banks for over a decade.