If you are looking to buy a manufactured home in a rural area and you meet certain income and property requirements, a USDA loan for a manufactured home could be one of the best financing deals available to you — zero down payment, below-market interest rates, and 30-year terms.

But USDA loans for manufactured homes have specific requirements that not every home or borrower will meet. This guide explains exactly who qualifies, what the property requirements are, and how to apply.

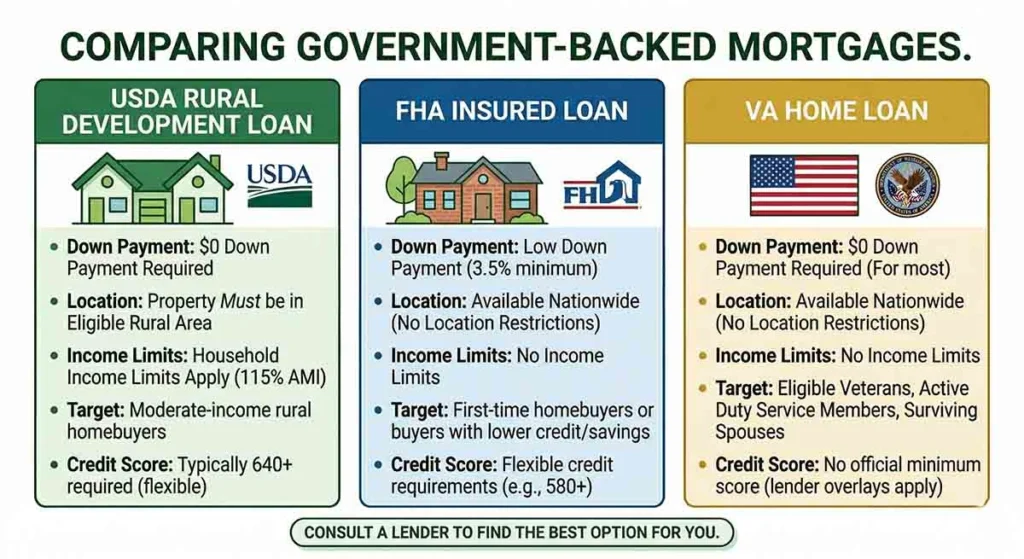

What Is a USDA Loan?

USDA loans are home loans guaranteed or offered directly by the U.S. Department of Agriculture through its Rural Development program. The program’s mission is to improve the economy and quality of life in rural America by making affordable homeownership accessible to low-to-moderate income families in eligible rural areas.

There are two types of USDA loans:

USDA Section 502 Guaranteed Loans

These are loans made by private lenders and guaranteed by the USDA. They are similar to FHA loans in structure — you apply through a USDA-approved private lender, and the USDA guarantees the loan against default. Most USDA manufactured home loans are of this type.

USDA Section 502 Direct Loans

These are loans made directly by the USDA to very-low and low-income borrowers who cannot obtain conventional credit. Interest rates can be subsidized down to as low as 1% for the most financially challenged borrowers. Direct loans are less commonly available and have stricter income limits than guaranteed loans.

Key Benefits of USDA Loans for Manufactured Homes

- Zero down payment: USDA guaranteed loans allow 100% financing with no down payment required

- Below-market interest rates: USDA rates are typically competitive with FHA rates and sometimes lower

- 30-year fixed terms: Long amortization period keeps monthly payments lower

- No PMI — but guarantee fee applies: USDA loans have an annual guarantee fee (0.35% of the loan balance) instead of PMI, which is typically lower than FHA MIP

- Flexible credit requirements: 640 minimum for automated underwriting, lower with manual underwriting

USDA Income Limits: Do You Qualify?

USDA loans are income-limited programs. To qualify for a USDA guaranteed loan, your household income cannot exceed 115% of the median income for your area. This limit applies to your total household income — all earning members of the household — not just the borrower’s income.

USDA income limits vary by location and household size. In 2026, typical income limits for a 4-person household range from approximately $110,000 in rural areas with lower median incomes to $130,000 or more in rural areas near higher-cost metro areas.

To check the income limit for your specific area, use the USDA’s online income eligibility tool at eligibility.sc.egov.usda.gov. Enter your address and household size to get the specific limit for your location.

Direct loan income limits are stricter — typically 50 to 80% of area median income, depending on the specific sub-program.

USDA Property Eligibility: Is the Location Rural Enough?

Properties must be in USDA-eligible rural areas. The USDA defines rural broadly — many areas that feel suburban are technically eligible. As a general guide:

- Open country and rural areas: Almost always eligible

- Small towns and communities (typically under 10,000 to 20,000 population): Often eligible

- Towns up to 35,000 population that are not adjacent to metro areas: May be eligible

- Suburban areas adjacent to major cities: Generally not eligible

- Major cities and their suburbs: Not eligible

Check the USDA’s property eligibility map at eligibility.sc.egov.usda.gov to confirm whether a specific address qualifies. Many buyers are surprised to find that properties they thought were too suburban are actually USDA-eligible.

USDA Manufactured Home Requirements

Not every manufactured home qualifies for USDA financing. The home must meet all of the following requirements:

HUD Code Compliance

The home must have been built on or after June 15, 1976, meeting HUD Manufactured Home Construction and Safety Standards. The HUD certification labels (red tags) must be present on the home.

Permanent Foundation Required

The USDA requires the manufactured home to be permanently affixed to a foundation that meets HUD’s Permanent Foundations Guide for Manufactured Housing. The home must be on land the borrower owns or is purchasing — park-based chattel homes do not qualify for USDA loans.

Real Property Classification

The home must be classified as real property — not personal property. If the home has a personal property title, it must be converted to a real estate deed before USDA financing can close.

No Wheels, Axles, or Hitch

The transportation undercarriage must have been removed.

Minimum Size

The home must be at least 400 square feet in floor area.

New vs. Used Homes

USDA guaranteed loans can be used for both new and existing manufactured homes. However, existing manufactured homes must be in good condition and typically cannot have any major deferred maintenance or structural issues. A USDA appraisal will evaluate the home’s condition as part of the loan process.

Credit Score Requirements

USDA loan credit requirements for manufactured homes:

- 640+: Eligible for automated underwriting approval — the standard, faster path

- 580 to 639: May qualify with manual underwriting, which requires more documentation and takes longer but is possible

- Below 580: Generally not eligible for USDA financing

Even with a score above 640, a USDA underwriter will review your full credit history. Recent bankruptcies (within 3 years), recent foreclosures (within 3 years), or significant derogatory items can complicate or disqualify an application even with an acceptable score.

Debt-to-Income Requirements

USDA guidelines generally allow:

- Front-end DTI (housing expense): 29% or less of gross monthly income

- Back-end DTI (all debt payments): 41% or less of gross monthly income

Manual underwriting may allow slightly higher DTI ratios with compensating factors (strong credit history, significant cash reserves, stable long-term employment).

USDA Guarantee Fee

Like FHA’s MIP, USDA loans have a guarantee fee that funds the program:

- Upfront guarantee fee: 1% of the loan amount (can be financed into the loan)

- Annual fee: 0.35% of the remaining loan balance, paid monthly

The annual fee is lower than FHA’s annual MIP (which ranges from 0.55% to 1.05%), making USDA loans less expensive on an ongoing basis than FHA for eligible borrowers.

Finding USDA-Approved Lenders for Manufactured Homes

Not all USDA-approved lenders offer manufactured home loans. As with FHA manufactured home loans, you need to find lenders with specific experience in USDA manufactured home transactions. Ask potential lenders directly whether they close USDA loans on manufactured homes and how many they have done in the past year.

Lenders that are active in rural markets — regional banks, credit unions, Farm Credit institutions, and rural-focused mortgage companies — are more likely to have USDA manufactured home experience than large national banks.

How to Apply for a USDA Manufactured Home Loan

- Verify income eligibility at the USDA’s online tool

- Confirm the property location is in a USDA-eligible area

- Check your credit score and resolve any issues

- Find a USDA-approved lender with manufactured home experience

- Get pre-approved — this clarifies your budget and shows sellers you are ready to buy

- Find a qualifying manufactured home on eligible land

- Complete the USDA appraisal and any required inspections

- Close on the loan

The Bottom Line

For eligible buyers in rural areas, a USDA loan for a manufactured home is an exceptional financing option — zero down payment, competitive rates, and 30-year terms. The income limits are generous enough to include middle-income buyers in rural areas, and the property eligibility map covers a larger portion of the country than many people realize.

If you are considering a manufactured home in a rural or small-town location, always check USDA eligibility before assuming it does not apply to you. Many buyers who assumed they would need an FHA or chattel loan have found that USDA financing was available — and better.

Marcus T. Webb is a former bank loan officer with 14 years in manufactured home lending. He has originated FHA, VA, USDA, and chattel loans across North Carolina and Tennessee. Today he writes about manufactured home finance to help buyers avoid the costly mistakes he watched happen in banks for over a decade.