Walk through any manufactured home lender’s inventory or search online and you will find them — repossessed manufactured homes, often listed at prices well below market. Repo manufactured homes can be genuine bargains, but they can also be financial traps if you do not understand exactly what you are buying and what risks come with it.

This complete, honest guide tells you everything you need to know about buying a repossessed manufactured home in 2026.

What Is a Repo Manufactured Home?

A repossessed manufactured home is one that a lender has taken back after the borrower defaulted on their loan — either a chattel loan (for a home in a park) or a mortgage (for a home on owned land). The lender repossesses the home and then typically tries to sell it to recover their outstanding loan balance.

Repossessions happen for various reasons — job loss, divorce, medical bills, and financial hardship are the most common. The previous owner’s financial problems are not your concern as a buyer, but the condition of the home very much is.

Where to Find Repo Manufactured Homes

Manufactured Home Lenders

The best source for repo manufactured homes is the lenders themselves. The two biggest specialized manufactured home lenders — 21st Mortgage Corporation and Vanderbilt Mortgage — maintain inventories of repossessed homes and list them on their websites. Both companies sell these homes and can also provide financing for qualified buyers.

Search “21st Mortgage repo homes” or “Vanderbilt Mortgage repo homes” to access their current inventory. These sites allow you to filter by state, price, and home type.

HUD Homes (For Real Property Manufactured Homes)

When a manufactured home financed with an FHA-insured loan goes into foreclosure, HUD takes possession and sells it through their HUD Homestore program (hudhomestore.gov). HUD homes are sold as-is, with no concessions, but are priced to sell — often below market value.

Bank and Credit Union REO Departments

Banks and credit unions that have made manufactured home loans maintain REO (Real Estate Owned) departments that manage and sell repossessed properties. Calling local banks and credit unions to ask about their manufactured home REO inventory can surface homes not listed publicly.

Online Marketplaces

Sites like MHVillage.com, Homepath.com (Fannie Mae), and Homesteps.com (Freddie Mac) list repossessed manufactured homes along with other distressed properties. Craigslist and Facebook Marketplace also periodically have private sales of homes that were previously repossessed.

Why Repo Manufactured Homes Can Be Bargains

Lenders are not in the business of owning homes — they want to recover their money and move on. This creates genuine motivation to sell quickly, which typically means:

- Prices set at or below appraised value rather than above

- Willingness to negotiate, especially for fast closings

- Potential for seller financing directly from the lender at reasonable rates

- No emotional attachment to the price — it is purely a financial transaction for the lender

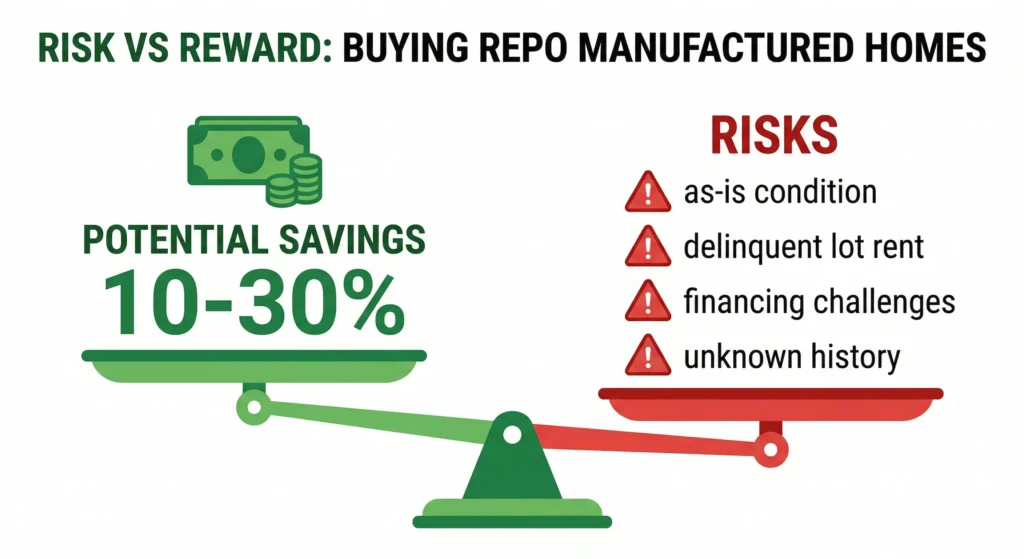

Savings of 10 to 30 percent below comparable market-rate manufactured home sales are realistic for repo purchases in many markets.

The Real Risks: Why Repo Manufactured Homes Can Be Traps

The potential savings come with real risks that every buyer must understand before making an offer.

Sold As-Is — No Warranty

Virtually all repo manufactured home sales are as-is, meaning the seller (the lender) makes no representations about the home’s condition and will not repair anything or provide any warranty. If the home has problems — and many do — those problems become your problems the moment you close.

Condition Unknown or Deteriorated

Repossessed homes often sat vacant for months or years before being sold. Vacant manufactured homes deteriorate quickly:

- Plumbing pipes can freeze and burst in cold weather

- Roof leaks go unaddressed and cause water damage throughout the home

- HVAC systems fail from non-use and lack of maintenance

- Vandalism and theft of copper plumbing, appliances, and fixtures are common in vacant homes

- Pest and rodent infestations establish in vacant structures

- Belly board damage from deferred maintenance allows moisture and pest entry

Delinquent Lot Rent (For Park-Based Homes)

If the repossessed home is in a mobile home park, the previous owner likely stopped paying lot rent before or during the repossession process. Outstanding lot rent may be owed to the park and could create a lien or access problem that you inherit as the new owner. Always verify the lot rent status with the park management before purchasing a repo home in a park.

Financing Challenges

Financing a repo manufactured home can be more difficult than financing a move-in-ready home. Lenders will appraise the home in its current condition, and a home with significant deferred maintenance may appraise below the purchase price or fail to qualify for certain loan programs entirely.

Some repo homes — particularly those that have been vacant for years — may only qualify for cash purchase or very high-rate hard money loans because they are not in financeable condition under FHA, VA, or USDA standards.

How to Evaluate a Repo Manufactured Home

Always Get a Professional Inspection

Never purchase a repo manufactured home without a professional inspection by an inspector with specific manufactured home experience. The as-is nature of these sales makes inspection even more critical than in a standard transaction. Budget $250 to $500 for the inspection — it is the most important money you will spend in this process.

The inspection should cover:

- Roof condition and evidence of leaks

- Floor system — check carefully for soft spots and water damage

- Plumbing — run every faucet and flush every toilet, check under all sinks

- Electrical — check panel condition, look for exposed wiring, test outlets

- HVAC — have the system evaluated by an HVAC technician if it has been sitting

- Foundation condition (for homes on land)

- HUD certification labels — confirm they are present

- Belly board condition

- Signs of pest or rodent infestation

Get Repair Cost Estimates Before Making an Offer

Once you have the inspection report, get cost estimates for all required repairs before making or finalizing your offer. Factor those repair costs into your total cost of acquisition — the purchase price plus repair costs is your real investment.

A repo home listed at $40,000 that needs $25,000 in repairs is not a bargain if a comparable move-in-ready home sells for $60,000.

Financing a Repo Manufactured Home

Your financing options depend heavily on the home’s condition:

- Move-in-ready condition: Standard manufactured home financing applies — FHA, VA, USDA, conventional, or chattel loan depending on the home’s title status and location

- Needs moderate repairs: FHA 203(k) rehabilitation loans can finance both the purchase and renovation costs in a single loan — worth exploring for homes that need work but are fundamentally sound

- Significant damage or condition issues: May require cash purchase, seller financing from the lender, or hard money financing until repairs are made and the home qualifies for permanent financing

Many of the major repo sellers — particularly 21st Mortgage — offer their own financing for repos they are selling. Their terms may be more flexible on condition requirements than conventional lenders, since they know the home’s history.

Negotiating on Repo Manufactured Homes

Lenders price repos to sell, but there is almost always room to negotiate — especially if:

- The home has been on the market for more than 60 days

- Your inspection found significant issues

- You can close quickly and pay cash or have pre-arranged financing

- The home is in a market with abundant repo inventory

A starting offer of 10 to 20 percent below asking price, supported by documented repair estimates, is a reasonable negotiating position. Lenders will not accept unreasonably low offers, but they are pragmatic — they want to close and recover their money, not negotiate indefinitely.

The Bottom Line

Repo manufactured homes can be genuine bargains for buyers who do their homework — verify the title, get a thorough inspection, price out repairs honestly, and negotiate from a position of knowledge. But as-is sales of homes that may have been vacant and deteriorating for extended periods carry real financial risk that can easily eliminate the apparent savings if significant repairs are needed.

Go in with eyes open, budget for contingencies, and never fall in love with a repo home until after your inspector has signed off on its condition.

Rafael Medina is a two-time manufactured home buyer who went from a 611 credit score and $8,000 savings to owning two manufactured homes — one in a park and one on private land with an FHA mortgage. He writes for first-time buyers and park residents, covering the practical, real-world side of manufactured home ownership from someone who has lived every step of it.